Hello

I'm Jellen Vermeir

Freelance IT and Data Science Consultant

- Company Essential Data Science Consulting ltd.

- Phone (+32) 473 47 48 59 / (+359) 894 80 11 34

- E-mail jellenvermeir@essentialdatascience.com

- Next Stops San Jose, Costa Rica / Auckland, New Zealand

- Min. Rate 1000€+/day (or startup equity)

- Weekends Only

Hi, my name is Jellen. I wear many different hats in life: I’m a computer engineer, a data scientist, a technology investor, a cryptocurrency trader, a micropreneur, an AI-fanatic and a healthcare & biotech enthusiast. I’m fascinated by technological progression and I enjoy getting things done. Feel free to drop me a line if you would like to discuss something.

Professional Summary

Jellen graduated as a computer engineer and subsequently completed several high impact government projects as a business analyst. Jellen then made a career shift towards quantitative finance and obtained an additional degree in financial and actuarial engineering. He completed this advanced education track while simultaneously working on his personal startup projects related to algorithmic trading and quantitative fund management.

Jellen has recently founded Essential Data Science Consulting ltd. and is currently providing high profile consultancy services towards the industry as a data scientist and/or quantitative analyst. He’s also venturing into the exciting new world of blockchain technology and cryptocurrency network security.

Areas of Expertise

Open Source, Open World

Stackoverflow - R / Python Data Science Support

During the previous years, I offered some -very minor- community support on stackoverflow by answering data modeling related questions. It is my intention to restart these efforts in a more serious manner very soon. My focus will most likely remain on R, but I would like to contribute to the Python community as well.

You can find my SO profile on this page.

PoloniexR - Cryptocurrency Trading Package

The PoloniexR package provides a convenient user interface to the Poloniex (Cryptocurrency Trading) REST API.

The package was committed to CRAN and the first version of the corresponding CRAN reference manual can be found on this page. At the time of writing, some documentation fixes are still required.

From a user perspective, more intuitive package installation instructions and tutorials can be found in this blogpost. The source code can be obtained from the following Github page.

Poker Handevaluation System

View Github for project details and demo.

This project provides a custom implementation of a Texas Hold ’em handevaluation subsystem as described in chapter 5 of the original Loki Poker Bot research paper. For preflop play, fixed relative strength values are provided based upon simplified monte carlo simulations where all players call to the end of the hand. For postflop play, calculations are provided to determine immediate handstrength and future handpotential via complete scenario enumeration (given the opponent hand probability distributions as input).

From this handevaluation system, betting strategies can be derived and opponent models can be added to provide more realistic and adaptive hand probability distributions. The university of Alberta Computer Poker Research Group has performed extensive research on both fronts and has succesfully used Poker as a testbed for AI and reinforcement learning techniques.

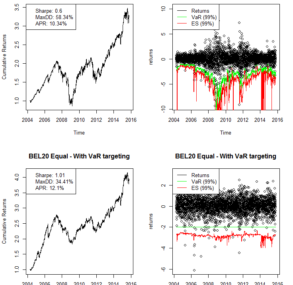

Financial Risk Modeling - Research Project

View Github for project details and demo.

In the paper and demos on Github we focus our attention on the risk modelling aspects of the portfolio management process. We first offer some motivational examples on why one should stay clear of the normality assumption while assessing portfolio risk. Stylized facts of univariate and multivariate financial market data are illustrated and discussed. We follow up with a few definitions and interpretations of financial risk and focus our attention to the Value at Risk (VaR) and Expected Shortfall (ES) measures. In the remainder of the paper we present alternatives to the normal distribution for modelling and forecasting the latter risk measures:

- We give an exposition on the Generalized Hyperbolic Distribution (GHD).

- We introduce methods and concepts from extreme value theory (EVT) as a means of capturing severe financial losses.

- Conditional risk measurements are presented in the form of GARCH models.

- Copulae are discussed with the purpose of modelling multivariate dependencies between assets.

From a more practical point of view we perform out of sample backtests and run statistical tests to evaluate the risk forecasting performance of the models. Here, we argue that a mixed (E)GARCH-Clayton/Gumbel copula model is especially suitable for asset return modeling and risk forecasting at the portfolio level. We demonstrate how the latter tool can be employed to provide superior risk adjusted returns in a portfolio context by reliably targetting a certain expected VaR (or ES) level during the portfolio rebalancing process.

Cointegration-Based Statistical Arbitrage Trading Strategy

View Github repository for paper and demos. This project consists of a proof of concept and conceptual demo of a simple stat-arb trading strategy that is based upon cointegration method.

Financial Engineering Toolkit

View Github for project details an demos.

This Matlab based Financial Engineering Toolkit contains several smaller subprojects in the domain of Financial Engineering and the Structuring of Financial products. Available subprojects:

- Pricing, Greeks, implied volatility of barrier options under Black-Scholes.

- Pricing, Greeks, implied volatility of Lookback options under Black-Scholes

- Stock path simulation under Black-Scholes and Heston

- Yahoo Option Chain Downloader

- Heston Calibration Toolkit

- Structuring of a Reverse Convertible (Paper and Demo)

METATRADER 4 - BACKTEST AND EXECUTION FRAMEWORK

View Github repository: This mql4-framework consists of a few dedicated modules that are linked together in order to assist the user with rapid prototyping and testing of simple TA forex strategies. An example expert advisor is also added for demonstration purposes.

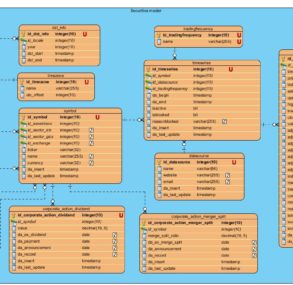

SECURITIES MASTER DATABASE

View Github repository: This project includes scripts that can be used to set up a basic securities master database. The database structure is fairly generic in the sense that it can contain data for any assetclass type and/or datafrequency. Additionally, the project includes scripts for the downloading, parsing and inserting of timeseries data for the S&P500 stocks, SPDR ETF funds, the BEL20 stocks and its corresponding ETF tracker. Simple scripts for data cleaning, outlier detection and corporate action backadjustment are provided as well.

Actuarial Statistics Projects

View Github repository: This project contains a few smaller subprojects that lie in the domain of non-life insurance actuarial statistics. Each of the subprojects contains its own readme file with additional information regarding the added functionality. Currently added subprojects:

- Claim arrival modelling using poisson processes.

- Loss severity modelling using a spliced ‘body and tail’ approach

- Claim frequency modelling using Generalized Linear Models (GLM)

Industry Experience

2017

Essential Data Science Consulting ltd. (EssentialQuant)

Cryptocurrency Mining

Setting up a proof of work (PoW) cryptocurrency mining operation in Iceland: Obtaining competitive advantages due to the following factors:

- Geothermal & hydro-electric power (electricity).

- Cold climate (cooling).

- Fibre internet access (P2P communication).

Operational pipeline:

- Deploying a GPU-based mining farm (ASIC resistant hashing algorithms only).

- Using optimization tools for coin selection.

- Continuously selling new coins at market prices.

2017

Essential Data Science Consulting ltd. (ENI Trading & Shipping)

Consultant - IT / Data Science

Providing IT and data science support to the front office trading department of a commodity trading company. Responsible for end-to-end project delivery on both technical and modeling side.

Technical Achievements:

- Providing a Transparent User Interface to the Back-end Data Storage (R / Python).

- Implementation of a centralized model-deployment and backtesting framework.

Modeling Cases:

- Energy Demand Forecasting (Machine Learning and Time-Series Analysis).

- Mult-Step Constrained Gas Flow Routing (Mathematical Optimization and Graph Theory).

2014 - 2016

Essential Data Science Consulting ltd. (EssentialQuant)

Quantitative Researcher

Researching, developing and deploying the EssentialQuant RiskResTrained Hedge Fund (Private investment fund, managed by Essential Data Science Consulting ltd.)

Obtaining deep technical exposure to the complete algotrading R&D pipeline:

- Strategy Development

- Risk Management

- Portfolio Optimization

- Reference Data Handling

- Execution Modeling

2012 - 2015

Smals VZW (Deployed at RVP)

Business Analyst Consultant

Preparing and coordinating the production execution of the Belgian governments' mission critical and deadline sensitive mass adaptations (Indexations, holiday money calculations, retirement benefit payouts etc)

Academic Background

Awards and Achievements

Received the Belfius Thesis Award for writing the best Master’s thesis in the Financial and Actuarial Engineering program. The research involved the development of risk management components that allow for accurate predictions of portfolio level risk metrics.

Contact Jellen

Send me a message

- E-MAIL jellenvermeir@essentialdatascience.com

- PHONE & WHATSAPP (+32) 473 47 48 59

- SKYPE EssentialQuant

- TWITTER @EssentialQuant

- COMPANY ADDRESS Moskovska str. 21B fl. 3, 1000 Sofia, Bulgaria

- CURRENT LOCATION Complex Sunset ap. 170, 8253 Kosharitsa, Bulgaria